- Value Investor Daily

- Posts

- Value Investor Daily #29

Value Investor Daily #29

Lululemon (LULU) Down 42%, PE at 10-Year Low, What’s Going on and Can The Stock Recover?

Lululemon Athletica (NASDAQ: LULU) has experienced a significant decline in its stock price, dropping over 42% from its peak to levels not seen since 2020.

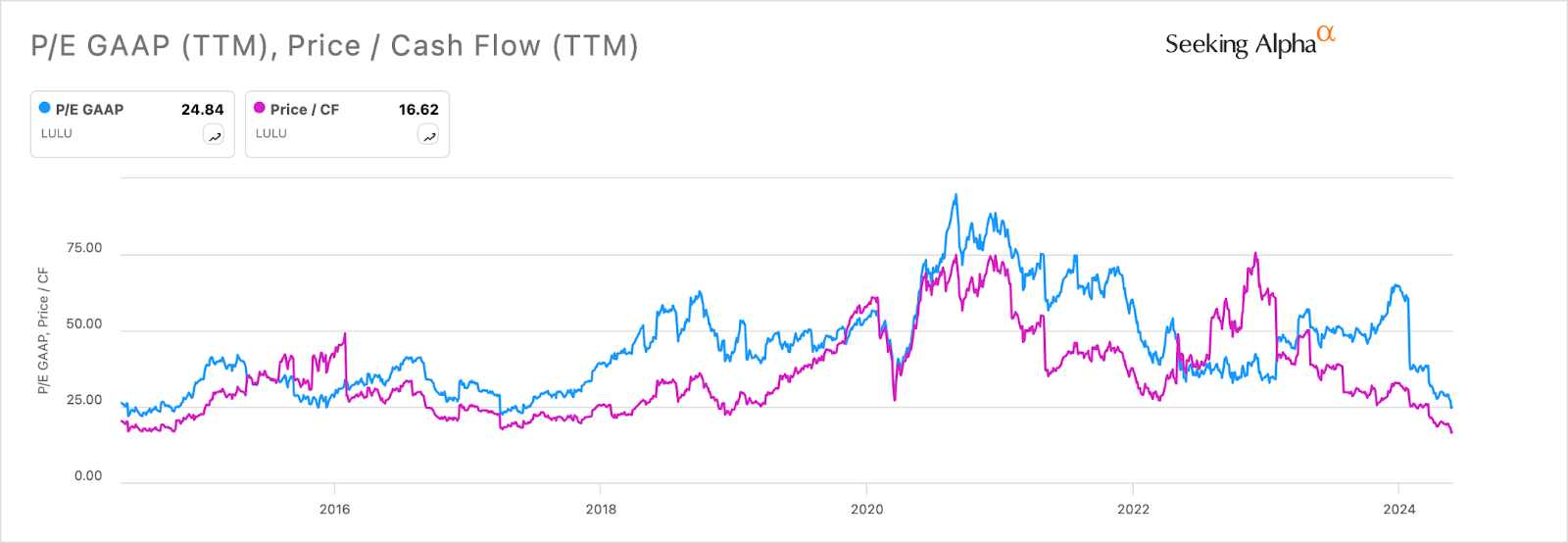

P/E and Price-to-Cash-Flow are at 10-year lows.

Source: SeekingAlpha

The drop comes in the wake of its Q4 earnings report on March 21st.

The company's lower growth outlook, influenced by slowing trends in the U.S. market, has sparked concerns about its market share potential.

Investors are increasingly anxious amid rising competition, changing consumer preferences, and evolving spending habits.

Let’s examine whether the stock selloff is excessive and if the current dip presents a buying opportunity.

Recent Developments and Strategic Shifts

Last week, Lululemon's shares fell nearly 10%, furthering the decline that began in March after announcing that Sun Choe, the Chief Product Officer since 2018, will be stepping down.

In response to Choe's departure, Lululemon outlined plans to restructure its organization, signaling a strategic shift in its management approach to better navigate internal and market dynamics.

Lululemon introduced significant organizational changes aimed at improving its product design and go-to-market strategies.

Jonathan Cheung, the Global Creative Director, will now report directly to CEO, eliminating an organizational layer to streamline the scaling of design ideas.

Additionally, Lululemon has formed a new team by merging leaders from its Merchandising and Brand functions.

Nikki Neuburger was promoted to Chief Brand & Product Activation Officer, highlighting the company's efforts to enhance its global and regional go-to-market strategies.

Challenges in the U.S. Market

Lululemon has struggled to maintain its growth momentum in the U.S. market.

In March, the retailer reported North American sales growth of 9% in Q4, a sharp decline from the 29% growth seen in the same period last year and down from 12% in the previous quarter.

This slowdown underscores the challenges Lululemon faces amid rising competition and changing consumer preferences.

The company indicated that its first-quarter sales in the U.S. have been sluggish.

CEO Calvin McDonald noted a recent shift in U.S. consumer behavior, with more shoppers opting for cheaper alternatives due to elevated inflation and high interest rates.

As Lululemon's dominance in the athleisure market faces increasing competition, price-sensitive consumers may shift their spending to more affordable brands.

When asked about US growth on the latest earnings call, here’s how CEO Calvin McDonald and CFO Meghan Frank responded:

Calvin McDonald:

Yes. Thanks, Matt. Definitely, still view across all markets being early innings in our growth story. When we look at Americas, as I mentioned, Canada is continuing its strong momentum into quarter one. And within the U.S., we're navigating what we see as a dynamic retail environment and a consumer that's a little bit softer, but there are a lot of areas that we are focused on and we know can continue to drive our business. That being product innovation and the unaided awareness, which in the U.S. is still very, very low. I think combined, it's less than 50%, in the 40% range with a lot of exciting initiatives planned to continue to make progress on that awareness metrics.

So, when we look across the metric, when we look across our categories, which I've always talked to you before in terms of the balanced approach across men's and women's and accessories and the pipeline and the ability to grow and where we are from an awareness perspective, no change in U.S., no change in our strategy. And with this guidance, not only did we complete 2023 ahead of our Power of Three x2 goal, but with the guidance, 2024, we will still be ahead of our Power of Three x2 goals, and we don't see a change in that.

Meghan Frank:

And Matt, I'll just add. We shared our long-term target of low double-digit CAGR for North America. We're tracking ahead of that to date in our plan, and feel comfortable with that long-term target. And then from a sales per square foot perspective, the U.S. is the highest in terms of sales per square foot by store. So -- and was continued to grow when we went through 2023, so we still feel like stores are important part of that strategy.

Opportunities in International Markets and DTC

Despite these challenges, many Wall Street analysts see significant growth opportunities in Lululemon's global business, which accounts for around a fifth of its total sales.

International sales momentum, particularly in China, is expected to remain strong, helping to offset near-term challenges in North America.

Analysts believe Lululemon's robust international presence and solid financial fundamentals provide a basis for sustained investor confidence.

When asked about e-commerce growth on the latest earnings call, here’s what the CFO had to say:

Meghan Frank:

Yes. So we have shared when we set out this Power of Three x2 plan that we expected e-com to grow slightly ahead of our CAGR of 15%, sales CAGR in stores is slightly below. I would say, over the long term time period, that view hasn't changed. We've seen, I would say, strength in both channels, coming off of 2023 e-com total growth 17%, stores 21%, e-com comp at 17%, and stores at 9%. So continue to see opportunity across both channels and leveraging that omni ecosystem.

Profitability

Despite the growth headwinds, the underlying business continues to be highly profitable.

TTM Revenue - $9.61B

TTM Net Income - $1.55B

TTM Cash Flow - $1.48B

LULU | TTM | 5Y Avg |

|---|---|---|

Gross Margin | 58.31% | 56.39% |

Net Margin | 16.12% | 14.17% |

FCF Margin | 15.45% | 8.98% |

Return on Equity | 42.01% | 34.65% |

Return on Capital | 28.00% | 24.51% |

Valuation

Utilizing an extensive range of valuation models, including P/E Multiples, Earnings Power Value, EV/EBITDA Multiples, 10Y DCF EBITDA Exit, and 5Y DCF Growth Exit, Lululemon's fair value estimate is determined to be around $393.

This suggests a nearly 30% potential upside from the current stock price.

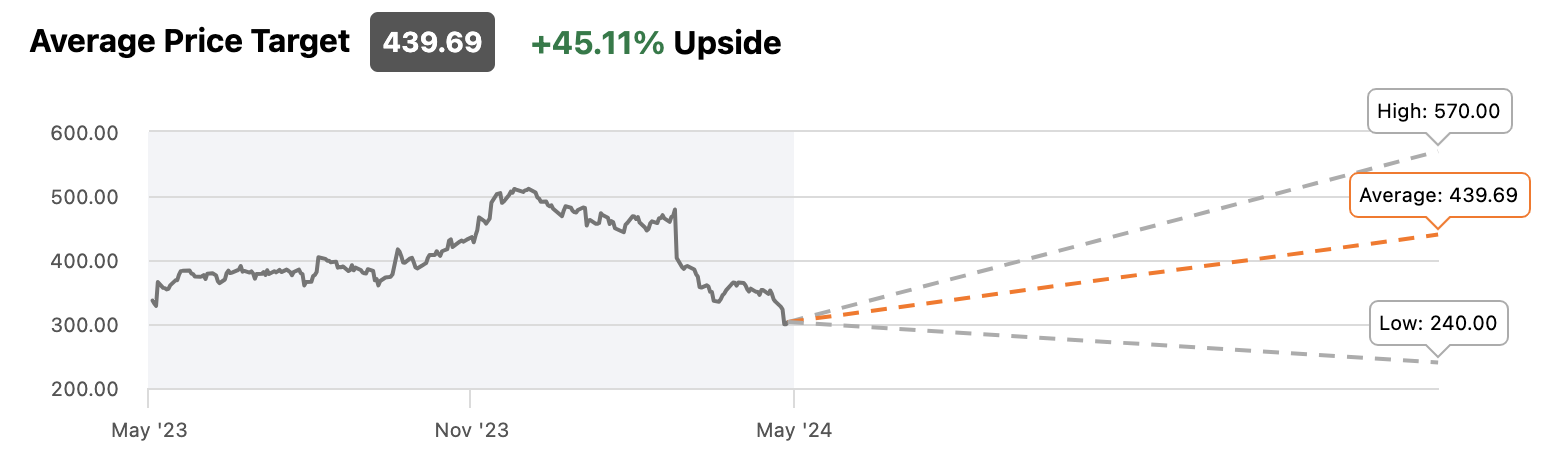

Analyst Perspective

Wall Street analysts also believe the stock is undervalued.

The average price target is $439.69, which implies a more than 45% upside potential from the present price level.

Source: SeekingAlpha

The company has $1.2 billion left on its current share repurchase authorization (vs. a market cap of $38 billion), so it could use the current drop in stock price to accelerate its buybacks.

It doesn’t pay a dividend.

Conclusion

While Lululemon faces significant challenges in its key U.S. market, the company's strong international presence and strategic management changes offer reasons for optimism.

Additionally, the fair value estimate and positive analyst perspectives suggest that the current stock selloff may present a buying opportunity for investors willing to look beyond short-term hurdles and focus on Lululemon's long-term growth potential.

Subscribe to our partners free: