- Value Investor Daily

- Posts

- Value Investor Daily #38

Value Investor Daily #38

XPEL Stock Is Down 58%, Is It Undervalued?

In partnership with

Take a demo, get a Blackstone Griddle

Automate expense reports so you can focus on strategy

Uncapped virtual corporate cards

Access scalable credit lines from $500 to $15M

XPEL, Inc. (Nasdaq: XPEL) has experienced substantial growth over the past five years, with a 33% CAGR in revenue. However, the year-over-year growth rate has recently slowed to 14.5% and is expected to decelerate to 8-10%.

The market cap is $1.18B.

The stock has fallen more than 58% since its July 2021 highs and is now trading at a P/E ratio of 25, compared to its five-year average of 48.

This analysis will explore the factors behind this decline, review the company’s financials, and estimate its fair value to determine if the stock is undervalued.

Company Overview

XPEL is a global leader in providing protective films and coatings, including automotive paint protection film (PPF), surface protection film, and window films.

The company commands around 40% of the U.S. PPF market, making it the largest player in this sector.

XPEL sources its products from a network of manufacturers and sells them to aftermarket installers and dealers.

Revenue Growth and Recent Slowdown

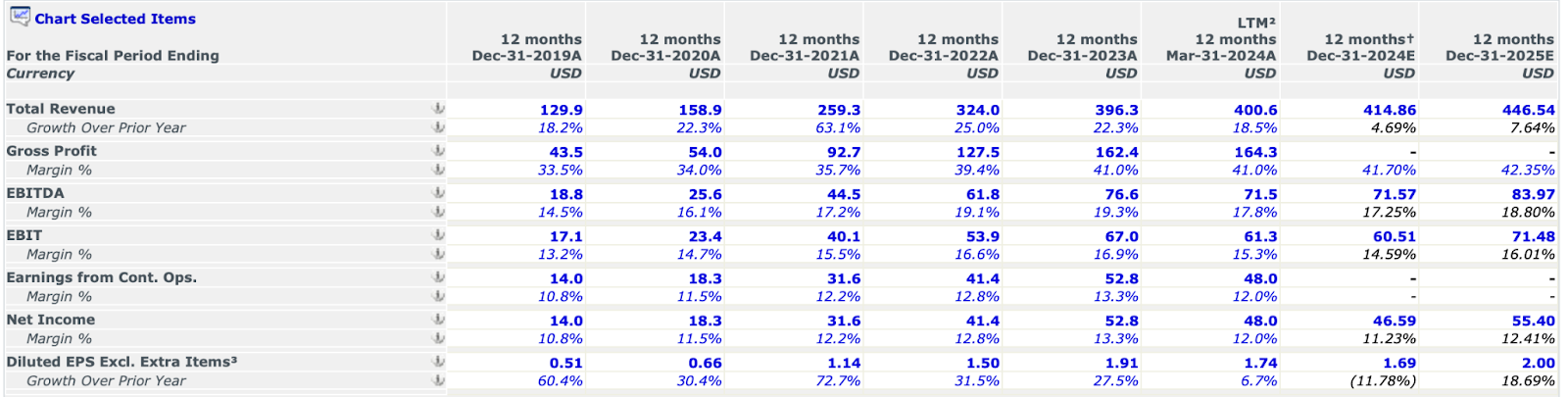

From 2019 to 2023, XPEL's revenue tripled from approximately $130 million to $396 million. However, this growth has slowed significantly, with projected revenue growth rates of 7.6% for 2024 and 8.1% for 2025. This deceleration follows an exceptional surge during the pandemic.

Source: CapitalIQ

Earnings

The company has missed consensus EPS estimates for three of the past four quarters.

XPEL’s Q1 performance was negatively affected by various macroeconomic factors, including a weakening consumer market, port delays that reduced sales of key brands like Porsche and Audi, and fluctuations in the Chinese market.

While the quarter's results were not disastrous, they fell short of the stellar performance investors have come to expect from XPEL in recent years.

Q2 has started to show signs of recovery. CFO Barry Wood highlighted the improvement in the latest earnings call:

Thanks, Ryan, and good morning, everyone. As Ryan mentioned, our total revenue grew 7.5%, but I think the China noise kind of masked the solid performance in the U.S. Ryan referred to the fact that our U.S. business posted a rather anemic 1.9% growth in Q1. So it was really nice to see the U.S. return to near double-digit growth in Q2, and this was on a tough comp as Q2 was the U.S. highest revenue quarter last year. So we are certainly encouraged by that.

Looking a little bit more detail on the product lines. Combined product and cutbank revenue increased 2.8%, where solid U.S. performance, again, was mostly offset with the impacts from China. Excluding China, combined product and cutbank revenue increased 7.8% in the quarter, and sequentially, combined product and cutbank revenue grew 24.1%.

Our window film product line revenue grew 8.4% quarter-over-quarter $22 million, which represented 20% of our total revenue. Excluding China, total window film revenue grew 18.6%, and sequentially, total window film revenue grew 51.3%.

Our Q2 vision product line revenue, which is included in our total window film revenue grew 29.6% to $3.1 million and represented 14.1% of our total window film revenue and 2.8% of our total revenue.

Our OEM revenue grew 23.6% in the quarter and represented 4.1% of total revenue. And our total installation revenue, which combines product and service grew 33.9% in the quarter and represented approximately 21% of total revenue, and this was really buoyed by strong performance in our OEM and dealership services businesses.

While the company is still projecting 8-10% revenue growth this year, pockets of the business are still experiencing aggressive double-digit growth.

Risks and Opportunities

Despite recent challenges, XPEL's financials remain strong. The company exhibits solid fundamentals, with consistent growth in revenue and profit margins and robust operating cash flow.

The balance sheet is also in good shape, with a debt-to-equity ratio of 15.5%.

In the near term, however, XPEL faces risks from a potentially slower macroeconomic environment and decreased visibility into factors that could negatively affect the adoption of aftermarket PPF in the U.S.

However, international expansion presents a significant revenue growth and diversification opportunity, particularly in rapidly growing markets such as China and India.

Here’s CEO Ryan Pape on acquisitions:

On acquisition front, we did close two acquisitions recently in June. We closed on the purchase of Protective Film Solutions, or PFS, based in Orange County, California. PFS, amazing brand. It has been an amazing brand ambassador for XPEL. But separate and above from how they're traditionally known in the automotive space, PFS has developed a substantial marine model for protection and application of a variety of products into the marine channel. And we intend to make that available in a structured way to our installer base over the next year for our installers that see that as a viable part of your business.

We see marine is another adjacent market and complementary market worth developing, and this is the first part of the investment to help kickstart that. Ryan Tounsley is the principal of that business, has joined us as our Director of Marine to spearhead the initiative. And as you know, it's all about the team in terms of what we can accomplish. So we're glad to grow in that direction.

Just this week, we closed on a small acquisition of our distributor in India. At the end of last year, we established our own operations in India, as we previously talked about, and our distributors' business will merge in with this operation. And as we discussed in the past, we want to be direct presence in the top car markets of the world, and this acquisition helps us further check that box. We expect to complete another four or five distributor acquisitions in key markets in Asia and Latin America over the next year. As we complete these, we will have a direct presence in the majority of the top 20 car markets in the world.

This CEO and business are still in high growth mode. But they’re highly economy-sensitive and solely dependent on the auto industry.

If the economy has a soft landing and interest rates continue to fall as the Fed starts to lower rates, it could set up XPEL for a continued earnings acceleration as the consumer rebounds from a break in borrowing costs.

If we have a hard landing, all bets are off; auto sales will get whacked, and XPEL’s business will slow down, too.

Valuation

According to Seeking Alpha's quant rating, XPEL has recently moved from a Strong Sell to a Buy rating. It considers several factors: valuation, growth, profitability, momentum, and revisions.

SeekingAlpha

Analysts estimate 9-30% earnings growth over the next 3-5 years, compared to 38% in the last ten years.

Let’s assume 17%, which aligns with the cash flow growth rate of 16.7% over the last three years.

According to our DCF, that implies a fair value of $52, a 21% margin of safety, compared to the current $41.65 price.

That would put earnings at $8.21 by 2034 and a stock price of around $205, a 17% CAGR if the P/E stays at today’s 25x.

Conclusion

While recent earnings misses and slower growth are concerns, XPEL's solid financial foundation and growth potential suggest a positive long-term outlook.

As always, do your own research and decide.

Thanks for reading today!

Take a demo, get a Blackstone Griddle

Automate expense reports so you can focus on strategy

Uncapped virtual corporate cards

Access scalable credit lines from $500 to $15M